Introduction

Beverage distribution in 2025 looks nothing like it did five years ago — functional drinks, ready-to-drink cocktails, and a rebounding on-premise channel have redrawn the competitive map. With RTD cocktail volumes projected to grow 400% from 2019 to 2029 and functional beverages like energy drinks posting 8% value growth in 2024 alone, choosing the right distribution partner has never been more consequential for retailers, bars, and restaurant operators.

With hundreds of regional and national distributors competing for the same shelf space and supplier contracts, identifying which ones are worth partnering with means looking beyond scale alone. The distributors that matter in 2025 distinguish themselves through technology adoption, portfolio depth across emerging categories, and the agility to respond to rapidly shifting consumer demand.

The U.S. beverage market now sits at $213.4 billion with a projected 3.4% CAGR through 2029. The companies on this list are positioned to grow with it — and to bring their partners along.

Key Takeaways

- The U.S. beverage distribution sector is expanding alongside surging demand for functional, health-forward, and RTD beverages

- Top distributors span wine & spirits, beer, non-alcoholic, and specialty health beverage categories

- Standout distributors in 2025 use AI-driven forecasting and digital ordering platforms to outpace slower competitors

- Don't choose on price alone — service consistency and category expertise matter more long-term

- Independent operators often find better fit with regional wholesalers that offer hands-on, personalized service

The State of Beverage Distribution in 2025

Beverage distributors serve as the critical middle tier in the U.S. three-tier system, which legally separates manufacturers (Tier 1) from retailers (Tier 3) to ensure tax collection and prevent monopolies. This system governs most alcoholic beverage distribution, while non-alcoholic products flow through more varied direct and third-party models.

The U.S. beverage market reached $213.4 billion in 2024 and is projected to grow at 3.4% annually through 2029, fueled by category-level shifts that are reshaping distributor strategies. Three growth areas stand out:

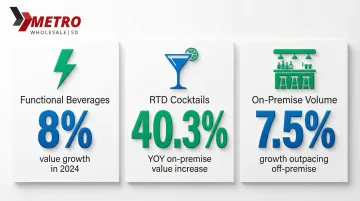

- Functional beverages (energy drinks, sports drinks, adaptogens) grew 8% in value during 2024

- RTD cocktails posted a 40.3% year-over-year value increase in on-premise channels

- On-premise volume grew 7.5%, significantly outpacing off-premise gains

These shifts have forced distributors to diversify portfolios, invest in cold-chain logistics for RTD products, and deploy digital tools that help retailers forecast demand for fast-moving categories. The five distributors profiled below have responded to these pressures in ways worth paying attention to in 2025.

Top 2025 Beverage Distributors to Watch

These five distributors were selected based on market presence, portfolio breadth, 2025 strategic momentum, and relevance to businesses sourcing across beverage categories.

Southern Glazer's Wine & Spirits

Southern Glazer's Wine & Spirits (SGWS) is the largest wine and spirits wholesaler in the United States, operating across 47 U.S. markets with international reach spanning Canada, the Caribbean, and Latin America. The company earned Beverage Industry magazine's 2025 Wholesaler of the Year award, recognizing its leadership in both scale and innovation.

Digital Platform & Commercial Strategy:

SGWS's proprietary Proof digital ordering platform has become an industry benchmark, generating approximately $4 billion in revenue in 2024. In California, nearly 20% of on-premise sales now flow through Proof, demonstrating how digital self-service is reshaping buyer behavior. The platform integrates AI-powered forecasting and personalization tools that help retailers anticipate consumer demand and optimize inventory.

Beyond technology, SGWS employs its PACE commercial planning process to help suppliers bring consumer-led innovations to market faster. Recent acquisitions signal deliberate geographic expansion: the Horizon Beverage Group acquisition added Massachusetts and Rhode Island, while the pending Anheuser-Busch NYC distribution operation deal strengthens its position in the nation's largest metropolitan market.

| Geographic Reach | 47 U.S. markets plus Canada, Caribbean, Central and South America | | Key Product Categories | Wine, spirits, RTD cocktails, malt beverages, non-alcoholic | | What to Watch in 2025 | AI-driven Proof platform expansion and New York City market launch |

Reyes Beverage Group

Reyes Beverage Group (RBG) is the largest beer and malt beverage distributor in the United States, delivering approximately 320 million cases annually to over 115,000 retail accounts across 35+ states. While anchored by Anheuser-Busch InBev brands, RBG is rapidly diversifying into high-growth categories.

Total Beverage Expansion:

RBG's massive logistics infrastructure and cold-chain delivery capabilities position it to capitalize on the RTD explosion. The company is moving decisively beyond traditional beer — in February 2025, RBG announced a major partnership with Brown-Forman to distribute Jack Daniel's & Coca-Cola RTD in California and secured distribution rights for Tito's Handmade Vodka in the same state.

Earlier moves added Monaco Cocktails — the #2 spirit-based RTD in the Midwest — to its Illinois and Indiana portfolios.

These moves reflect RBG's strategy to become a "total beverage" distributor, capturing share in premium spirits and RTD cocktails while maintaining its beer dominance. For retailers seeking a single distributor for both traditional malt beverages and emerging RTD categories, RBG's portfolio breadth now covers more categories than any comparable beer-focused network.

| Geographic Reach | 35+ U.S. states with national-scale logistics | | Key Product Categories | Domestic and import beer, hard seltzer, RTD cocktails, malt beverages | | What to Watch in 2025 | Expansion into emerging RTD and better-for-you malt categories |

Breakthru Beverage Group

Breakthru Beverage Group operates across 14+ U.S. markets and Canada, focusing on premium wine and spirits distribution with a supplier portfolio that includes Diageo, Brown-Forman, and other luxury brands. In May 2025, Breakthru was named Brown-Forman's largest national distributor partner, covering 14 key markets across North America.

Data-Driven Portfolio Intelligence:

Breakthru's competitive advantage lies in data analytics and commercial intelligence. The company developed a "Lost Sales" dashboard in partnership with Slalom and Snowflake, using predictive analytics to quantify potential revenue lost due to out-of-stocks. This tool enables better inventory planning for on-premise accounts, directly addressing a pain point that costs bars and restaurants significant revenue during peak periods.

Breakthru's curated approach to portfolio management favors depth over breadth, making it particularly relevant for premium-tier retailers and hospitality buyers who prioritize quality over volume. Strong relationships with national restaurant and hospitality chains give Breakthru an edge in the recovering on-premise channel, where volume growth of 7.5% is outpacing off-premise gains.

| Geographic Reach | 14+ U.S. states and Canadian markets | | Key Product Categories | Premium spirits, wine, champagne, luxury RTD | | What to Watch in 2025 | Data-driven portfolio curation and on-premise growth strategy |

Keurig Dr Pepper (KDP)

Keurig Dr Pepper is a dominant force in non-alcoholic beverage distribution, combining its own brand portfolio—Dr Pepper, Snapple, 7UP, Core Hydration—with distribution agreements that extend its reach into energy drinks, functional beverages, and coffee. KDP's direct-store-delivery (DSD) network services over 190,000 retail outlets and covers approximately 80% of the U.S. population.

Co-Distribution Scale & Emerging Brand Access:

KDP's strength lies in its ability to co-distribute third-party brands alongside its owned portfolio, providing emerging brands with immediate national reach. In 2024, KDP announced distribution agreements for Electrolit and C4 Energy, and acquired GHOST lifestyle energy brand, bolstering its position in the fast-growing energy and functional hydration categories.

The DSD model gives KDP unmatched access to convenience stores, grocery, and food service at scale, with over 6 million annual customer sales visits. For non-alcoholic category buyers focused on energy, functional, and better-for-you beverages, KDP's co-distribution model means shelf placement decisions made through one partner can reach 80% of the U.S. consumer base.

| Geographic Reach | National U.S. coverage through owned and partnership DSD networks | | Key Product Categories | Carbonated soft drinks, energy drinks, water, coffee, functional beverages | | What to Watch in 2025 | Expanded energy and functional drink co-distribution partnerships |

KeHE Distributors

KeHE is a leading specialty and natural food and beverage distributor serving retailers across North America, with a portfolio heavily weighted toward organic, functional, and better-for-you beverages. Operating 19 distribution centers and servicing more than 31,000 retail accounts, KeHE specializes in sourcing and scaling emerging brands before they enter mass retail.

Functional & Natural Category Depth:

KeHE's strength lies in identifying and distributing the next generation of functional beverages — kombucha, adaptogen drinks, plant-based milks, prebiotic sodas — categories posting some of the fastest growth in the current market.

In September 2025, KeHE expanded its partnership with Total Wine & More to become the primary distributor for specialty grocery categories nationwide, extending its retail footprint considerably.

KeHE is the distributor that independent natural retailers and health-focused chains rely on to stay ahead of trends. Its January 2025 partnership with Plus Brand to distribute Agua Plus alkaline water exemplifies its focus on functional hydration. With 31,000+ accounts and 19 distribution centers, KeHE reaches health-conscious shoppers at a scale few specialty distributors can match.

| Geographic Reach | North America-wide with 19 distribution centers | | Key Product Categories | Natural/organic beverages, functional drinks, kombucha, plant-based, specialty water | | What to Watch in 2025 | Functional and adaptogen beverage category acceleration |

How We Chose These Distributors

This list was built for retailers, restaurants, and independent operators who need to know which distributors are actually performing well in 2025.

A few common mistakes buyers make: choosing a distributor based on brand name alone, overlooking service territory limits, or underestimating the importance of minimum order flexibility.

Key evaluation factors considered:

- Serves your region with reliable delivery infrastructure

- Supplies both traditional staples and emerging categories like RTDs and functional beverages

- Offers digital ordering platforms, analytics tools, and predictive ordering tools

- Investing in health-forward and functional beverage categories for 2025

- Actively growing through acquisitions, new supplier partnerships, or territory expansion

These criteria narrow the field, but the right fit still depends on your specific situation. Category focus, order volume, service channel (on-premise vs. retail), and location all shape the decision. Premium spirits buyers will prioritize very different partners than convenience store operators stocking energy drinks and functional waters.

Conclusion

The best beverage distributor for your business in 2025 isn't necessarily the largest—it's the one with the right portfolio depth, reliable service cadence, and the flexibility to grow with your operation. As consumer preferences continue shifting toward functional beverages, RTD cocktails, and better-for-you options, your distributor's ability to keep pace with those shifts affects what you can put on shelves and when.

When evaluating distributors, track ongoing performance across these core metrics:

- Fill rates and order accuracy

- Delivery consistency against committed schedules

- Responsiveness to reorders and urgent requests

- Ability to introduce new SKUs that match shifting consumer demand

The distributors profiled here demonstrate these capabilities at scale. That said, regional and local wholesalers often provide the flexible minimums and hands-on service that independent operators need to compete.

For San Diego-area retailers sourcing beverages and consumer packaged goods in case-pack quantities, Metro Wholesale is a local B2B wholesale option worth considering. Contact them at info@metrowholesalesd.com or call +1 619 423 5600 to discuss your ordering needs.

Frequently Asked Questions

What is the difference between a beverage distributor and a beverage wholesaler?

While both operate between manufacturers and retailers, distributors typically manage logistics, sales representation, and market development for brands, whereas wholesalers primarily buy in bulk and resell without the added sales or brand-building role. In practice, the terms are often used interchangeably, particularly in the alcohol industry where "wholesaler" is the legal term for the three-tier system's middle tier.

How do I choose the right beverage distributor for my business?

Start with these four criteria:

- Territory coverage and delivery frequency in your area

- Categories and brands they carry that match your customer base

- Minimum order requirements that fit your purchase volume

- Reputation for reliability — ask for references from similar businesses nearby

What types of beverages do wholesale distributors typically carry?

Most large distributors are category-specific: wine/spirits distributors like Southern Glazer's, beer distributors like Reyes, or non-alcoholic specialists like Keurig Dr Pepper. Regional wholesalers often carry a broader mix including soft drinks, water, juice, energy drinks, and specialty beverages. Specialty distributors like KeHE focus exclusively on natural, organic, and functional beverage categories.

What are typical minimum order quantities (MOQs) for beverage distributors?

MOQs vary widely. National distributors may require pallet-level purchases (20-50 cases), while regional wholesalers often offer case-level minimums (5-10 cases) more suited to independent retailers and small foodservice operators. Always confirm MOQs directly with the distributor, as they may vary by product category and delivery location.

How are 2025 consumer trends affecting beverage distribution?

Demand for functional beverages, RTD cocktails, and premium imports is pushing distributors to diversify their portfolios and add new supplier partnerships. Those that can't supply emerging categories like adaptogen drinks or hard seltzers risk losing shelf space to more nimble competitors.

What should small businesses look for in a local beverage wholesale partner?

Prioritize proximity for reliable delivery, flexible order sizes that avoid large upfront investments, and a product mix that fits your customer base. Beyond logistics, look for a partner who offers personalized support and can recommend products based on your specific sales patterns — not just a generic catalog.